One of the most confusing aspects of Project Management is the concept of Contingencies and Management Reserves. When are they used? What are they used for? And how are they applied?

In this article I will lift the veil.

Contingencies

Contingencies are amounts placed in the project estimate to account for “known unknowns.” That is, the existence of the cost is known, but the size of it is not. For example,

- In a house building project, the amount of design time is not known for sure.

- In a software development project, the cost of the database is uncertain because its specifications are not known for sure.

- In a bridge building project, the potential rise in streamflow could cause a rise in costs.

Thus, contingencies apply to costs that you know you must incur, but are not certain about their exact size.

Management Reserves

Management Reserves, on the other hand, are amounts placed in the estimate for “unknown unknowns.” That is, there are risks that have not been taken into account that might occur. For example,

- In a house building project, the draftsperson might quit, and a contract draftsperson must be hired at additional cost.

- In a software development project, the database might be hacked and cause an escalation in security costs.

- In a bridge building project, an airplane might crash into the project site.

As you can see, management reserves are risks that have not been accounted for in the estimate (an airplane might crash into the project!).

Management reserves serve as a catch-all for all other risks that are not specifically considered in the project estimate.

Many organizations track the cost escalation on past projects and allocate this to each future project as a Management Reserve. This can be either a percentage or a fixed fee.

Role of the Work Breakdown Structure

The Work Breakdown Structure (WBS) is the underlying basis for estimates. It contains a listing of tasks required to carry out the project, and it provides the foundation upon which to produce estimates. For example, a project task list might be:

| Work Breakdown Structure | |

|---|---|

| Task | Budget |

| Pound fence posts | $1,000 |

| Build fence | $2,500 |

| TOTAL | $3,500 |

Although not an ironclad law, the contingencies should be applied at the task level, and the management reserves on the project level.

For example, if the cost of the fenceposts is uncertain, this would be a contingency and you could add 10% to the task “Pound fenceposts.” However, to account for the possibility of a plane crashing into the fence during construction, you would add a 10% management reserve to the overall project.

Role of the Risk Register

The project Risk Register is used to gather information that determines the size of contingencies and management reserves.

The Risk Register records the risks to the project’s success factors. It also determines the priority of each risk, which is based on the risk’s severity and probability of occurrence. For example, an airplane crashing into the construction site is probably not the most important risk.

| Risk Register | |||

|---|---|---|---|

| Risk | Probability | Severity | Contingency |

| Stream flow rises – requires construction of larger berm | 10% | $10,000 | $1,000 |

| Site foreman quits | 5% | $10,000 | $500 |

| Airplane crashes into site | 0.001% | $100,000 | $100 |

| TOTAL | $115,000 | $1,600 | |

The contingency is estimated by multiplying the Probability with the Severity, and added to the applicable task estimate for the project.

Notice that in this example, since these three risks are all included in the project estimate they are all contingencies. The third item, an airplane crash, would normally be considered too remote to include as a contingency and would be included in the management reserve for the project.

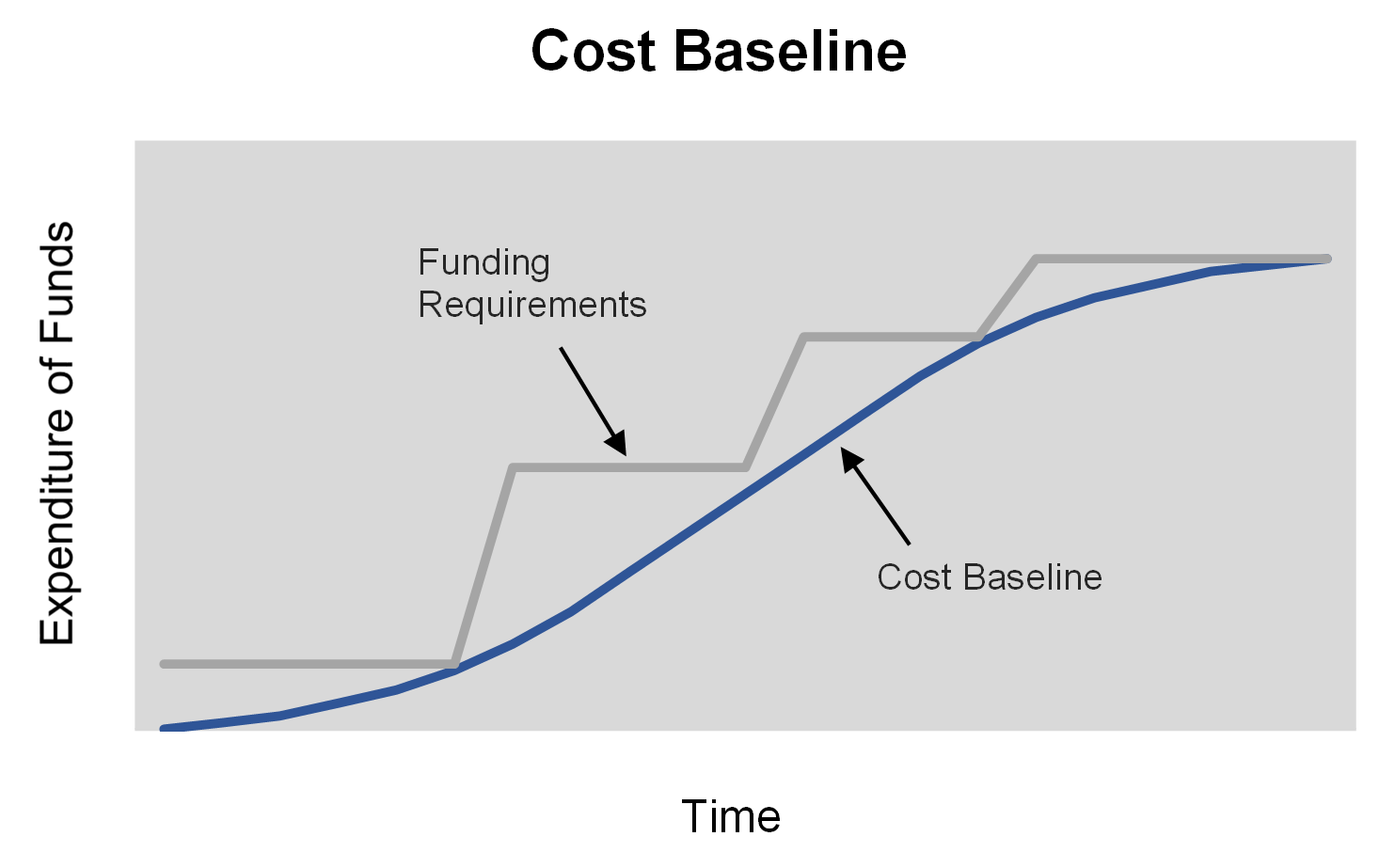

Cost Baseline

The cost baseline represents the time phased expenditure of project funds. It includes the contingencies, but not the management reserves.

The cost baseline represents the time phased expenditure of project funds. It includes the contingencies, but not the management reserves.

That is, management reserves are considered over and above the project budget and must be applied for separately from organizational management.

Cost Management Plan

The Project Management Body of Knowledge (PMBOK) specifies the use of a Cost Management Plan, which is a component of the overall Project Management Plan. This Cost Management Plan should contain the following information:

- How much contingency to include in each task

- Quantity of Management Reserve to include in the entire project

- Methodology, assumptions, and/or background information