Once the tasks within the project have been defined, the resources required by each task must be determined. To do this, we consult the PMBOK’s Estimate Activity Resources process.

PMBOK, 5th Edition, Section 6.4, “Estimate Activity Resources”

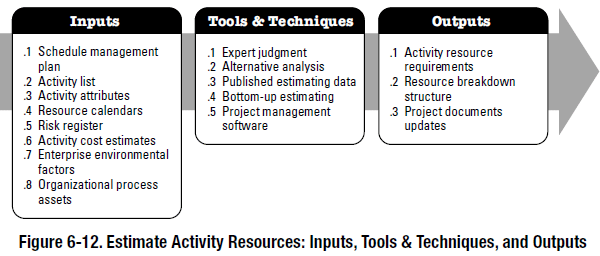

Estimate Activity Resources is the process of estimating the type and quantities of material, human resources, equipment, or supplies required to perform each activity. The key benefit of this process is that it identifies the type, quantity, and characteristics of resources required to complete the activity which allows more accurate cost and duration estimates.

Estimating Techniques

Generally you would perform tasks estimates from the bottom up, meaning each task is given an estimate which is then rolled up into the overall project estimate. Naturally, this is called Bottom Up Estimating. Within each task then, you can employ one (or more) of three estimating techniques:

- Analogous Estimating. This is when you make an analogy to the same, or similar, task that has been performed before. This is the best source of information because actual work completed, even if it requies adjustments, is extremely reliable. For example, if your project is for building a driveway and you’ve done it before, you clearly have a head start. Oftenyou have to make some adjustments, but the starting point is tremendously valuable.

- Parametric Estimating. In this method the work is drilled down into a unit cost, for which an estimate exists from published data or prior experience. For example, the cost per square foot of log home can be gleaned from previous projects. In the engineering industry almost everything is done this way, from the engineering time down to the construction materials.

- Three point estimating. If you’re not sure but can readily put an upper and lower bound on the value, this method is for you. With a three point estimate you choose an optimistic (a) and pessimistic (b) estimate in addition to the normal, most likely (m) one. Then a distribution can be chosen to arrive at the final estimate.

- Normal distribution: te = (a + m + b) / 3.

- Beta distribution: te = (a + 4m + b) / 6.

A resource calendar is consulted to determine if the resource is available. This can be a simple listing of when Bill or Mark will be on vacation or occupied on another job site. Or it can be an actual calendar within software that manages the workforce of an organization. Although the exact placement of each task is determined at the very end of the scheduling process using a technique called resource levelling (described at the end of this tutorial) at this point it is sometimes beneficial to consult the resource calendar to make sure the schedule isn’t seriously out of whack due to resource availability.

Types of Resources

At this stage each task on the task list is scrutinized and the resources required to perform the task are identified. For small projects there are four major types of resources:

- Labor

- Tools & equipment

- Material & supplies

- Fixed cost items like subcontractors, etc.

Labor

Accountants divide labor into three categories:

- Direct. Work that results in production units. The hourly unit rate of a laborer, or a salary divided into the number of days or hours they work on the project. It must also include benefits, retirement contributions, bonuses, and any other expense associated with the employee.

- Indirect. Work that is required to produce deliverables but doesn’t directly translate into production. This includes things like quality control, production supervision, and yes, project management. This type of labor needs to be included in estimates to give an accurate project cost. It needs to be divided into each task and allocated as much as practical.

- Overhead. Organizational administration costs like CEO’s salaries are not attributable to the project but, depending on the organizational structure, sometimes must be paid for by all projects. Normally the organizational administration (non-project) expense is calculated yearly and divided among the number of employees to arrive at a unit rate which is added to the direct labor rate.

Usually an established labor cost will be known to the company. If not, start with the direct labor and make the necessary allocations for indirect costs.

Tools & Equipment

This category generally includes all of the items that do not go into the finished product. Things like drill bits that are used up during a project, or the addition of new tools that the company doesn’t already own, and equipment such as software, forklifts, and excavators.

Often the tools and equipment will be used over multiple projects. In this case it is important to divide the cost over a conservative amount of projects to get a realistic idea of how much the project is “paying” for it. Conservative means a low number of projects – You want to make sure you are justifying the cost of the equipment.

Materials & Supplies

This includes the items that become part of the finished product, like timber for a log home or gravel for the driveway. Often these items are quoted by the unit, such as per foot of timber. Normally you have to calculate the exact quantity and include a bit extra, for things like:

- The material is not produced in the exact lengths required.

- The project will generate some waste.

Once those factors are taken into account, a contingency factor of 10% (more or less) can be applied to arrive at the final estimated quantity.

Where there are many small supplies it is generally recommended to include a catch-all item like “Landscaping Supplies.”

Fixed Cost Items

Often everything else can be lumped together into fixed cost items.

For example, subcontractors are a common requirement which must be tracked under each task. But be careful to read the fine print or you might discover the hard way that it isn’t as “fixed cost” as you think. Contracts, by definition, identify a scope of work and a price associated with it, and in every industry that I know of contractors can, and do, regularly request “scope changes.”

Other Resources

For larger projects, or where greater project management effort is justified, the following resources can also be used.

- Organizational/Administration. The portion of the organization’s administration cost that the project must pay for.

- Facilities. The purchase or rental of buildings to perform the work.

- Financing costs. The interest cost for loans required to carry out the project.

- Contingencies. Where the complexity of the project justifies contingencies as separate resource items, they can be tracked separately.

- Overtime pay. This applies to people as well as to equipment who’s rates increase after a certain point in time.

Example

An example resource list for a log house project might look like this. It is broken down into tasks and each task is assigned resources, to whom quantity and cost estimates are produced.

| 110 – Excavation | ||

|---|---|---|

| Type | Average Use | Total |

| Excavation Contractor | 30 hrs @ $180/hr | $5,400 |

| Bob | 10 hrs @ $45/hr | $450 |

| TOTAL | $5,850 | |

| 120 – Pour Foundation | ||

|---|---|---|

| Type | Average Use | Total |

| Concrete Forms | Lump Sum | $1,000 |

| Bob | 20 hrs @ $45/hr | $900 |

| Mark | 40 hrs @ $35/hr | $1,400 |

| Bill | 40 hrs @ $35/hr | $1,400 |

| TOTAL | $4,700 | |

| 210 – Wood work | ||

|---|---|---|

| Type | Average Use | Total |

| Timber | 1,200 m @ $35/m | $42,000 |

| Crane | 2 days @ $70/day | $1,400 |

| Other Supplies | Lump Sum | $5,000 |

| Bob | 90 hours @ $45/hr | $4,050 |

| Mark | 120 hrs @ $35/hr | $4,200 |

| Bill | 120 hrs @ $35/hr | $4,200 |

| TOTAL | $60,850 | |

| 310 – Electrical & Plumbing | ||

|---|---|---|

| Type | Average Use | Total |

| Electrical Contractor | Lump Sum | $8,700 |

| Plumbing Contractor | Lump Sum | $11,200 |

| Bob | 16 hrs @ $45/hr | $360 |

| TOTAL | $20,260 | |

| 320 – Flooring | ||

|---|---|---|

| Type | Average Use | Total |

| Flooring Contractor | Lump Sum | $18,400 |

| Bob | 8 hrs @ $45/hr | $360 |

| TOTAL | $18,760 | |

| 330 – Finishing | ||

|---|---|---|

| Type | Average Use | Total |

| Finishing Contractor | Lump Sum | $16,400 |

| Bob | 8 hrs @ $45/hr | $360 |

| TOTAL | $16,760 | |

| 410 – Landscaping | ||

|---|---|---|

| Type | Average Use | Total |

| Bobcat | 8 days @ $65/day | $520 |

| Other Supplies | Lump Sum | $2,000 |

| Bob | 20 hrs @ $45/hr | $900 |

| Mark | 60 hrs @ $35/hr | $2,100 |

| Bill | 60 hrs @ $35/hr | $2,100 |

| TOTAL | $7,620 | |

Therefore, once all of the individual tasks are added up the total cost for the log house is:

| Task Budgets | ||

|---|---|---|

| ID | Task | Cost |

| 110 | Excavation | $5,850 |

| 120 | Pour Foundation | $4,700 |

| 210 | Wood work | $60,850 |

| 310 | Electrical & Plumbing | $20,260 |

| 320 | Flooring | $18,760 |

| 330 | Finishing | $16,760 |

| 410 | Landscaping | $7,620 |

| TOTAL | $134,800 | |